I like to make a fortune in 2022, and I will make a fortune every year!

This article is the original article of Value Firm, the 1013th article.The article only records the thoughts of Value Firm, which does not constitute investment advice. The author has no group, no charge for stock recommendation and no financial management on behalf of clients.

Everyone knows that medical treatment is an excellent track, with all kinds of 10-fold shares and 100-fold shares, but it is also recognized as complex and difficult to learn. Now, the course of medical investment, which is probably the best one you can find, is coming. The course combs the huge medical system and decomposes it into 15 sub-tracks, and then analyzes the investment opportunities of the sub-tracks one by one. Let you master the medical investment method from now on, know the investment logic of each track clearly, and seize the opportunity to learn.

special column

Quickly master the secret of medical industry investment in 21 days.

Author: Director of Value Firm

298 coins

248 people have bought it.

examine

Whenever the market falls, we feel that this decline will show a unilateral downward trend and continue, so we always cut our meat in the most desperate time; On the contrary, every time it goes up, we will feel extremely excited and think that it will keep going up, thus forgetting all risks and always rushing in when it goes up the most.

In fact, the market always runs periodically, but the presentation of each cycle is so different that everyone always mistakenly thinks that "this time is different", but the fact is that it is the same every time.

Looking at history, whether it is the history of the industry or the history of the big market, whether it is the big A in China or the Dow Jones in the beautiful country, the market or the good industry is always advancing in the waves.The cycle has never failed, never in the past and never will..

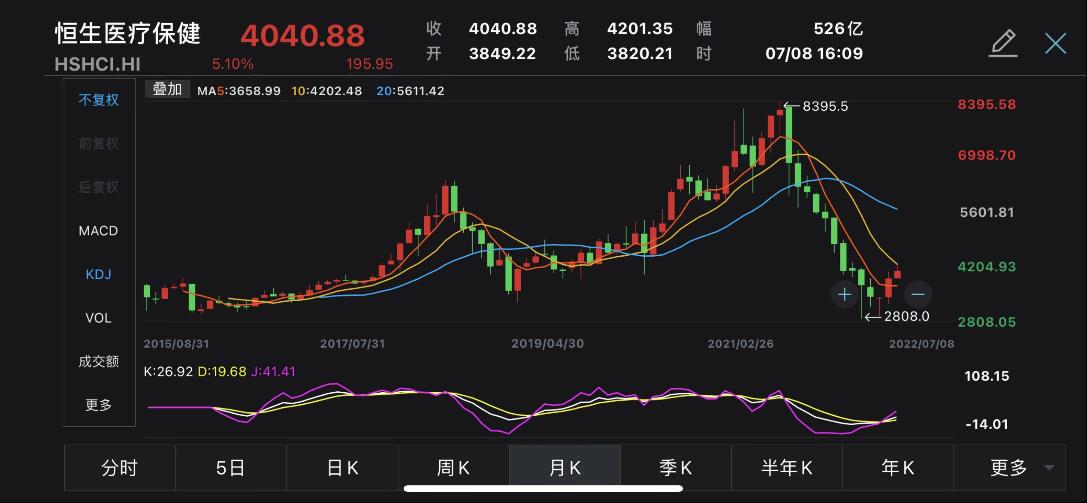

Take the pharmaceutical industry, which we are most familiar with, as an example. The chart below shows the Hang Seng Health Care Index, and the chart below shows two big cycles.

This is not only the case in Hong Kong market, but also if we look at the XBI index in the United States. If the decline in China is due to centralized purchasing in 2018 and innovative drug involution in 2021, then the synchronization of beautiful countries is unreasonable.

Jumping out of the past two cycles, in China, the medical industry also experienced an epic slump in 2015, when the fuse was July 22 verification.As long as it is a medicine, the clinic is all stopped.At that time, the pessimistic view in the market was that there was no way to go for pharmaceutical R&D in China, and there would be no future for pharmaceutical industry in China. After all, R&D was stopped, what else could we do?

Then, in the end, it turned out to be better. After the clinical crash in 2015, it created a vigorous bull market in 2016-2018, and after the collective purchase crash in 2018, it created a vigorous bull market in 2018-2021.

Therefore, everything is actually a cycle. For now, it is not our assets that have problems. It is purely because the environment is not good, and drinking cold water is full of teeth; For those who have risen sharply, it is often not that the assets are particularly good and investors have excellent eyes, but because the environment is too good and pigs are flying.

After understanding the theory of the cycle of everything, we can be more calm about the fluctuation of the market..

Then, the question comes, and many people sometimes ask the director, since we know that the cycle lasts forever and the cycle is repeated, why don’t we sell at the top of the cycle and buy at the bottom of the cycle?

If there is an expression, the director will definitely roll his eyes here and say, I really want to hit you.

Although on a large scale, the market always changes in cycles, the specific situation of each wave is different. For example, in the pharmaceutical industry this time, if you copy 2018 and fall for more than half a year, you will rebound violently, then you will lose. If you fall for half a year, you will be killed halfway up the mountain, and the wave of Hang Seng Medical has fallen through the bottom of the previous wave.

It is precisely because of such reasons that people mistakenly think that each cycle is invalid. In fact, it is not invalid, but the details are different.

The details include historical background, historical events of the trigger cycle, duration and fluctuation range. …….

For example, the last events that triggered a sharp decline in medicine included trade conflicts, centralized drug collection and economic downturn; This time, it is the epidemic situation, the conflict between Russia and Ukraine, the Fed’s interest rate increase and contraction, and the negotiation of innovative medicines. ….

Especially these historical events, how big are the influencing factors and how long will they last? God only knows, so, if you want to perfect the prediction cycle, it is as difficult as reaching the sky, it is too super-circle, and male and female servants can’t do it.

Since it is impossible to judge the inflection point of the cycle, what should we ordinary investors do?

Although we can’t predict the inflection point, we can deal with it, and we can give two ways to do it ourselves.

First, the simplest and easiest thing to do is to lie flat.

Although the cycle goes round and round, if we take a good industry and a recognized good company, we should add a word here.Don’t sneer at the so-called institutional conglomerates.In fact, the investment and research capabilities of institutions are really strong, and the enterprises that enable them to hold a group are basically enterprises with excellent comprehensive capabilities in all aspects.

In fact, the director doesn’t like the word "Bao Tuan" very much, but everyone likes to use it, so let’s use it. However, not only do we like "Bao Tuan" at home, but also overseas. All institutions in the world like those well-known companies, that is, Facebook, Amazon, Google, Apple, Microsoft, etc. They are really good, and their long-term returns are also very good.

In fact, in beautiful countries, if you don’t participate in these recognized good enterprises, but you won’t get any benefits, can you say that the whole world is holding a group?

Good enterprises are limited. As for the so-called collapse theory of conglomerates, most of the collapses actually come back and hit a new high, while a few collapses actually have problems with the underlying logic.

In short, most good enterprises have no problem lying flat, losing time, but not losing money. If the time is long enough, it is a highly probable event to beat inflation and increase the value of assets, such as Maotai, Yili, Midea, Hengrui, Mindray and other well-known big white horses.

Second, advanced, that is, the more you fall, the more you buy.

Real investment in big coffee will wait until the cycle is relatively bottom before making a move, and the first move is a big one, but few people have the patience and few people can do it. Everyone knows that it is undervalued and overvalued, but everyone can’t do it. The most likely situation is that many people can resist not making a move at PE40, 50 and 60 times, but eventually they make a move at 200 times.

Typical, such as the big bull market of consumer medicine in 2020, there are many people around the director who catch up with Maotai 70 or 80 times.

As Howard Marx said:There are always some determined bidders who will surrender in the late bull market..

However, it doesn’t matter if you buy high. As long as you dare to increase your position after falling, you can eventually flatten the cost. Big deal, rebound and then slowly reduce, to make up for our mistake of chasing high and buying.

For example, the director once failed in a transaction, because he really liked that company too much. Although he waited for it to fall back from a high position before entering, he was still at a high position overall. Later, it has been falling and falling, but it’s a matter of fact. The director has been buying and buying all the time. By the time he was in his thirties, he was even more heavy-handed, buying much more than all the quantities he bought before, and finally pulling the cost very low.

In recent months, it rebounded and immediately went up. Although the current price is far from the original 140+, the director still made money on the whole. Assuming that the enterprise goes back to 140+ or even exceeds that price, then the enterprise will bring at least several times the return to the director, which is a home run.

Of course, it’s easier said than done, but it’s actually very difficult. Don’t say that the more you fall, the more you buy. It’s good that most people can fall without cutting their meat, not to mention catching the "falling knife".

Moreover, according to the director’s experience, even if every time I feel overwhelmed and marvel at how such a low price can occur, there is a high probability that there will be a lower time. For example, in the above enterprise, the director made a heavy hand at 34.1, but actually the lowest fell to 31.4, which means that the company dropped by 10 points after the director made a heavy hand for the last time, and the director actually thought that it should be almost 70.

However, the director is still very happy. Although he failed to buy the lowest point, he also made up for the relatively low point, and he will be happy that he can bravely add positions against the trend, because the director deeply understands that,It is normal for the market to have huge volatility. Even the best industry/enterprise can’t go up every day (of course, a good enterprise/industry can’t keep falling). Moreover, the ultimate excess returns often come from a huge decline.. Those who go up as soon as they buy it are often lucky. Luck is the most unreliable thing.

Many people, although they know that floating losses are not losses and floating profits are not gains, know that fluctuations are the norm and that the wind and water turn around, but when they really fall into their own accounts, they still find it difficult to overcome their own psychological barriers.

Many times, it is not a cognitive problem, but a psychological problem. Just as the director said a "joke" in the value firm max: At this time last year, many friends asked me the question: Now that medicine is so expensive, can I still invest? During this time, more people ask: medicine has been abandoned, is it still worth investing?

Haha, do you find it contradictory and interesting?

In fact, this is the biggest difference between the market and the industry. For enterprises in the industry, there may be periodic ups and downs, but there is no such rapid and exaggerated change in the secondary market. The director himself is also an entrepreneur, knowing that a company or an industry can never change dramatically in a few months or a year.

Therefore, when the market is in the down cycle, the problem is more not at the enterprise level, but at our human nature level. Not long ago, I was in a good state of mind, clamoring for a new high. How long did it take this time, and when I fell, I began to worry about the enterprise? Ask yourself, is this a problem with the enterprise or your mentality?

Sometimes our enemy is not cognition, but weakness in human nature..

There are too many weaknesses in human nature, and the market seems to be a special place to punish human nature. As long as there is a weakness in your human nature, it will be exposed sooner or later, and then the market will double the punishment.

Therefore, the longer I stay in the market, the more I feel that doing a good job in value investment is actually a process that infinitely makes our humanity close to perfection.

So don’t always think about the perfect operation of maximizing benefits. Such operation doesn’t exist, or it doesn’t belong to you. Only the operation that infinitely approaches perfect humanity is possible.

Finally, I would like to give you a grand introduction: "Learning Value Investment from scratch" newly released by the team of value firms. This book is different from the existing investment books on the market. It is completely based on the perspective of novice investors and focuses on the puzzles that novices will encounter. In the book, the industry analysis, company analysis, valuation analysis, etc. are greatly simplified and combed into an analytical framework, so that Xiaobai can simply follow the reference analysis, just like tracing red when practicing pen writing.

After reading the book, Xiao Bai can also learn to do his own company analysis, instead of learning it at first sight and then wasting it. Friends who want to learn company analysis and value investment by themselves must buy a book and study it well.

Copyright statement: This article was originally edited and published by Value Firm. The data are all from public data, and some pictures are from the Internet. The copyright belongs to the original author. If there is any infringement or doubt about copyright, or exclusive information disclosure/content cooperation, please contact us by email.laoduo1995@qq.comWe will deal with it as soon as possible, thank you!

special column

Quickly master the company valuation method in 10 days.

Author: Director of Value Firm

138 coins

158 people have bought it.

examine

Learn value investment from scratch

¥69